Fee-Only Makes A Difference

Why Does Fee-Only Make A Difference?

Phillip James Financial is not your traditional financial planner. This is because of our compensation structure, called “Fee-Only.” This fee is based on the percentage of assets that we manage for you. This is different from most other financial planners who are compensated through commissions, loads, and charges. It’s this unique way in which we are paid that allows us to be objective in our advice and reduce conflicts of interest. As a “Fee-Only” registered investment advisor (RIA) we are legally held to a Fiduciary Standard, which means by law we have to hold your interests above our own. Learn more about the different compensation structures the associated conflict of interest, and the Fiduciary Standard below.

How an Investment Advisor is compensated is important.

Fee-Only Financial Advisors

As a Fee-Only financial advisor we charge our clients directly for our advice and the on-going management of their assets. We are completely transparent in our fees so you will always know what you are paying us. We receive no other financial reward from any other source. This means we never receive referral fees or commissions and therefore are not incentivized to push one product over another. We simply advise on the best investment for you situation. This compensation structure aligns our goals with yours, which is to grow your wealth.

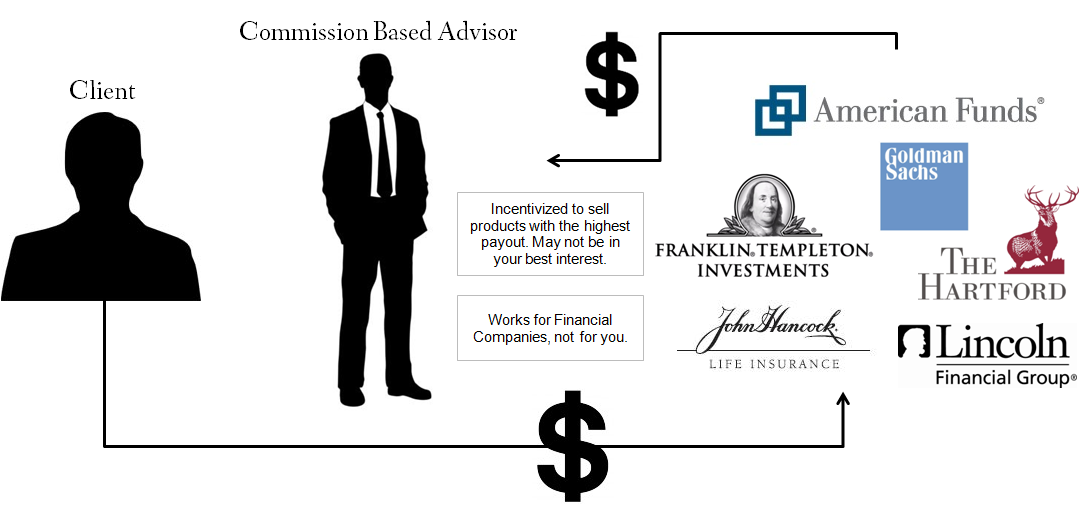

Commission Based Financial Advisors (Broker/Dealers)

When working with a commission based advisor, you don’t pay fees directly to the advisor, instead you pay the insurance companies and mutual fund companies whose products are sold by the advisor. These costs are in the form of various sales-charges (loads), commissions, and ongoing management expenses. The financial companies then pay part of this to the advisor. In the investment world these commission based advisors are often called “Broker/Dealers.” Broker/Dealers are really just financial salesmen because their goal is to sell you products which in turn provides them with their sales.

The problem isn't that the advisor is paid; the problem is that it creates a Conflict of Interest between the interests of the client and that of the advisor. The commissions provide an incentive to sell products with the highest payout to the advisor (e.g. loaded mutual funds, variable annuities, whole life insurance) regardless of whether or not this is the best option for the client.

Below are some charts which help illustrate the difference between the two compensation models.

The Fiduciary Standard

As a Fee-Only Financial Planner we are registered with the state of Minnesota (officially labeled a Registered Investment Advisor or RIA). Federal and state law requires that RIAs be held to a fiduciary standard. This requires us to act solely in the best interest of our clients at all times. We must disclose any conflict of interest, adopt a code of ethics, and fully disclose how we are compensated.

Unfortunately, only a small percentage of “financial advisors” are RIAs. Most so-called financial advisors like the Broker/Dealers mentioned above are not held to a Fiduciary Standard; they are instead, held to a lower Suitability Standard. In fact, they are required by law to act in the best interest of their employer, not in the best interest of their clients.

Because broker/dealers are not necessarily acting in your best interest, the SEC requires them to add the following disclosure to your client agreement. Read the disclosure, and decide if this is the type of relationship you want to dictate your financial security:

“Your account is a brokerage account and not an advisory account. Our interests may not always be the same as yours. Please ask us questions to make sure you understand your rights and our obligations to you, including the extent of our obligations to disclose conflicts of interest and to act in your best interest. We are paid both by you and, sometimes, by people who compensate us based on what you buy. Therefore our profits, and our salespersons’ compensation, mat vary by product and over time.”

If this disclaimer appears in the agreements you are signing, you are not working with a Fiduciary advisor. You should ask additional questions about how he or she is compensated, and where his or her loyalties lie. Then decide if the relationship is right for you.

Fee-Based ≠ Fee-Only

Fee-only planning has gained in popularity in the last few years because of its transparent compensation structure and because it removes the conflict of interest associated with selling a commission based product. This means more people are switching to these types of financial planners. In response, many commission based broker/dealers have attempted to get their share of the market back by offering fee-based planning in addition their commission based practice. This can be confused with fee-only but it is certainly not the same. Fee-based advisors charge clients a fee for their advice just like fee-only advisors but unlike fee-only they also may receive payments for the products they sell or recommend. In some cases commissions are credited towards the fee, giving the appearance of a lower-priced option, but any indirect compensation creates a conflict of interest and lessens the advisor’s ability to keep the client’s best interests first and foremost.

To experience the Fee-Only Difference for yourself Schedule a Meeting Online or Contact Us for more Information.